Ensemble Active Management: The Blueprint for Rescuing Active Management

[ad_1]

I. Introduction

Innumerable papers in recent years have explained why passive management is the heir apparent to traditional active management. This is not such a paper. Nor does it counsel patience in the mistaken belief that active management will soon reclaim its dominance. Without structural change, it cannot. In fact, the data presented here demonstrates that evolutionary advances will not improve active management’s inferior position relative to passive. The status quo has become a permanent trap for active managers.

But a solution exists. By applying proven best practices for predictive analytics from other industries to investing, Ensemble Active Management (EAM) could generate enough added alpha for active management to reclaim its edge over passive. The improvement is significant and differentiated enough for Ensemble Active to stand on its own as a third investing category alongside Passive and Traditional Active.

Active managers are inherently in the prediction business, which is very different from market timing. They forecast — based on research, analytics, experience, and skill — the stocks most likely to outperform. Other industries — weather forecasting, medical diagnostics, voice and facial recognition, credit scoring, etc. — have achieved substantive leaps in predictive accuracy. It is time for the investment industry to embrace the same methods.

EAM is not theory — it has been in live operation for two years — and EAM Portfolios are now commercially available to the public and have been validated by live market performance.

EAM is not a simplistic artificial intelligence (AI) alternative to traditional stock picking. It does not replace investment professionals with machines. EAM builds upon proven investment concepts and techniques, and then enhances them by applying modern predictive analytics.

Finally, EAM can operate at massive scale and has the potential to persistently outperform passive investing. It is a valid, viable, and achievable blueprint for retooling active management’s existing engines.

II. Defining the Problem

What percentage of active funds outperform their benchmark?

To find out, we used rolling one-year relative performance versus a fund’s benchmark as our primary metric and defined a fund’s “Success Rate” as the percent of those one-year periods when the fund beat its benchmark.

Success Rates over rolling time periods have several advantages for large data analyses. They don’t depend on a specific start or end date, and so are less subject to manipulation. They allow comparisons across different market cycles and asset classes, and among funds with both short- and long-term track records. They also help neutralize the impact of outlier months or quarters on overall performance assessments.

We defined a 50% Success Rate as a neutral result since investors had an equal chance of outperforming or underperforming. Thus 50% is the minimum threshold at the fund level. Since higher-fee active management must aim for more than just parity with passive, we defined 65% as the “target” Success Rate.

We analyzed performance data for all 1,813 US equity mutual funds classified by Morningstar as US Equity, non-index (i.e., actively managed), and with a published track record of at least one year. The cumulative assets under management (AUM) for these funds, as of November 2020, totaled $4.9 trillion.

We collected daily returns for these funds from January 2005 through November 2020, and then converted the data to rolling one-year returns. (For funds with inception dates earlier than 2005, there was a maximum of 3,755 rolling one-year periods). We determined relative performance by comparing the one-year fund performance to the corresponding Russell style and capitalization indexes. For example, the Russell 2000 Growth Index was the benchmark for funds classified Small Growth by Morningstar. This yielded 5.59 million data points.

The Results: Overall Assessment

Across all funds and all rolling time periods, the average Success Rate for the industry was only 41.6%. The Success Rates for all funds are aggregated on an annual basis in the following chart:

Annual Success Rates, US Equity, Actively Managed Funds

The trend is decidedly negative. Less than 1% of annual Success Rates exceeded 65%, and the average relative return underperformed by -89.4 basis point (bps), or -0.894%.

Active managers failed to achieve their mandate, and their performance is trending the wrong direction.

Next we evaluated Success Rates at the fund family level, focusing on the largest 50 firms based on actively managed US equity AUM. These firms have access to the top managers and investment infrastructure, and thus are theoretically most capable of generating persistent outperformance.

But only four of these fund families had an average Success Rate of 50% or above. The best average Success Rate was 56%.

Finally, we assessed Success Rates at the individual fund level, evaluating each fund over its entire track record. Only 25.9% of the 1,813 funds had a Success Rate of 50% or more, and just 4% of these had Success Rates of at least 65%.

Such data demonstrates why investors are voting with their feet. Since 2010, net outflows from actively managed US equity funds have totaled $1.6 trillion and $1.3 trillion since 2015. The pace of outflows is accelerating.

Quarterly Net Flows: Actively Managed US Equity and US Sector Equity Mutual Funds, 2005 to 2020

The Results: Quantifying the “Alpha Gap”

The findings thus far mirror conventional expectations that passive investing has had the upper hand for years. But what about the future outlook?

Is active’s relative underperformance structural? Will improvements in research and portfolio design and reasonable fee-cutting reverse the current competitive paradigm?

To answer these questions, we calculated how much added alpha would have been needed, on a per fund annual basis, for active funds to match their passive benchmarks and achieve the 50% minimum threshold and then reach the 65% target. We call this required excess return the “Alpha Gap.”

Alpha Gap Adjustments and Result Success Rates:

All Funds, Jan. 2005 to Nov. 2020

We calculated the Alpha Gap by adding a fixed amount of return to each fund, for each rolling one-year period, until the active management industry’s average Success Rate reached the targets. To achieve the 50% Success Rate, the average fund had an Alpha Gap of 94 bps. To reach 65%, the Alpha Gap was 267 bps.

Implications and the Path Forward

The lower hurdle appears out of reach, the higher target all but impossible. Therefore, active management’s competitive disadvantage is, indeed, structural.

Which brings the industry to a crossroads: It can either ignore the reality that a sustainable relative performance recovery is wishful thinking — the so-called “definition of insanity” approach — or step back, rethink, and re-engage through an improved paradigm.

EAM is that new paradigm.

III. Integrating Best Practices for Predictive Analytics into Investment Management

One of the best ways to solve an old problem is to reframe it.

For decades, the investment industry has approached the performance challenge by pre-imposing constraints. Every solution had to fit within the so-called “three-Ps” (People, Philosophy, and Process) model: a single manager/team, delivered as a discrete portfolio, with one defined philosophy and process. This necessarily limits the options available to solve the problem.

Such constraints and the “single-expert” paradigm are unique to the investment industry. The fund manager equivalent in other sectors would be defined as a single-expert predictive engine, designed to identify stocks that will outperform the market. These other industries have demonstrated that single predictive engines are suboptimal when it comes to solving complex predictive challenges. This is not conjecture, but settled science.

Why? Because of the Bias-Variance Conflict or Trade-Off. Bias occurs when the predictive model’s underlying assumptions are flawed or out of sync, and a “high bias” predictor will produce consistently off-target results (left-hand “target”). A “high variance” algorithm will deliver low accuracy results (right-hand “target”). At a certain point, efforts to reduce bias-related errors can dramatically increase variance errors and thus act as a hard ceiling preventing quality results.

Bias vs. Variance

This trade-off is depicted in the chart below. The point of lowest Total Error — the black line which equals the total Bias plus Variance errors — does not reach an optimal level of error reduction because as Bias error is reduced, Variance error increases exponentially, and vice versa.

The Bias Variance Trade-Off

Ensemble Methods are a subcategory of machine learning and were explicitly designed to solve the Bias-Variance Conflict. By analyzing the underlying single-expert forecasts and mathematically identifying areas of agreement, they build a more accurate “super predictive engine.”

Ensemble Methods are broadly viewed as a cornerstone of computational science. As Giovanni Seni and John Elder explain, Ensemble Methods are “the most influential development in Data Mining and Machine Learning in the past decade.”

For a real-life example of how another industry adopted Ensemble Methods to improve predictive outcomes, Appendix 1 below reviews the $1-million Netflix Prize

Defining Ensemble Active Management

Our three-step approach to building EAM Portfolios provides the key to unlocking structural, incremental alpha.

1. Assemble a multi-fund platform.

These funds are the source of the predictive engines used in constructing EAM Portfolios. There are, however, some important considerations for the selection of the underlying funds:

- All of the managers must share the same investment objective, such as beating a standard index like the S&P 500.

- Most of the fund managers need to demonstrate better-than-random stock-selection skill for at least their highest conviction picks.

- The investment processes must be independent. This is critical. Diversification at the predictive engine level is how Ensemble Methods solve the Bias-Variance Conflict.

2. Extract the “predictive engine” from each fund.

There is vast difference between a fund’s holdings and the predictive engine that selects those stocks. EAM processes operate through the predictive engines, or the decision frameworks, with which each fund manager selects stocks and determines daily weightings.

Since predictive engines are rarely accessible, their decisions are inferred or estimated through the forecasts embedded within a fund’s highest overweight and underweight positions relative to the benchmark. These are the manager’s highest conviction picks. A dynamic portfolio of each manager’s highest conviction security selections are then applied in constructing EAM Portfolios.

3. The extracted, underlying predictive engines are processed through an Ensemble Methods algorithm, which is then used to build an EAM Portfolio.

This final step, the application of Ensemble Methods to the underlying predictive engines, creates a new forecasting engine that is more accurate than the underlying approaches. The heightened accuracy creates additional alpha. The results detailed below demonstrate that the added excess return can be significant.

Ensemble Active Management vs. Multi-Manager Portfolios

An EAM Portfolio is not the same as a multi-manager portfolio.

Multi-manager portfolios (“MMPs”) have diversification benefits at the process level. This diversification, by definition, is a risk-management tool. It cannot generate incremental alpha. MMP performance is more stable than a single-manager’s performance, including reduced distribution curve tails. But MMPs reflect the combined holdings of all the underlying portfolios, so a multi-manager portfolio’s return always equals that of the weighted-average of the underlying portfolios.

In contrast, EAM Portfolios are derived from predictive forecasts extracted from single manager portfolios — not the underlying portfolios themselves or the largest holdings. They are built from the decision processes used to construct those portfolios. These predictive engines are then integrated through an Ensemble Methods algorithm to create a more accurate predictive engine.

This new engine generates an investment portfolio derived from the enhanced Ensemble Methods-based stock forecasts. The resulting EAM Portfolio will not contain all the stocks in the underlying single-manager portfolios, just those with the highest consensus from among those forecasts. The final mathematical output factors in both positive and negative forecasts as well as the degrees of manager conviction. EAM Portfolios can thus create additional alpha.

See Appendix 2 for an example of how an EAM Portfolio statistically compares to a multi-manager portfolio.

The distribution curves in the following chart demonstrate how these concepts work.

Impact of EAM on Hypothetical Distribution

- The Red Curve is a hypothetical distribution of the aggregate relative performance outcomes for 10 individual funds, each using traditional active management techniques.

- The Black Curve is the relative performance distribution of the same 10 funds blended into a multi-manager portfolio.

- The Green Curve is the hypothetical relative performance distribution of an EAM Portfolio built from the same 10 underlying funds.

The multi-manager design adds risk management, and thus reduces the size of the positive and negative tails compared to the single manager portfolios as demonstrated by the two “A” arrows.

The multi-manager portfolio does NOT add alpha. Thus the median return of both the Red Curve and the Black Curve represented by the vertical dotted red and black lines remains constant.

The Green Curve represents the alpha created by the EAM methodology, which results in a positive shift in the median returns: The “B” arrow moving from the black dotted vertical line, or median return of the traditional active portfolio, to the green dotted vertical line, or the median return of the EAM Portfolio.

Because of its multiple predictive engines, the EAM Portfolio also generates a residual risk-management benefit, with reduced tail distributions similar to a multi-manager portfolio.

IV. EAM Model Portfolios: Performance Validation

At the end of November 2020, 34 EAM Model Portfolios from 11 different firms were in live production, as tracked by Turing Technology. Each of these had to be based on a client’s design and codified through a contract and their track records are able to be validated and verified by an independent third-party. None of them were produced by Turing Technology. The firms that created them ran the gamut from boutique specialty shops to top-ranked insurance companies. The portfolios covered six distinct asset classes, Mid Cap Blend, for example. Nineteen have at least a 12-month history, with the oldest having a 23-month track record.

Performance Metric 1: Success Rates for Live EAM Portfolios

For the 19 EAM Portfolios with at least a 12-month history, there are 2,263 rolling one-year periods. Of those, EAM Portfolios outperformed their respective benchmarks 1,786 times, for an average Success Rate of 78.9%.

Model Portfolio performance is normally measured gross of fee. But for better comparisons to mutual funds, we reduced the annual return for each rolling one-year period by 85 bps to simulate the impact of fund fees. This slightly reduces the average Success Rate to 77.1%.

The comparison of EAM Success Rates to actively managed US equity funds and the two aspirational Success Rate thresholds referenced earlier are presented in the following chart. The EAM Success Rate is nearly double that of traditional actively managed funds and exceeded the 65% target Success Rate.

Success Rates: EAM vs. Active Fund Industry

The EAM Portfolios did not modestly outperform. The average annual excess return was 885 bps after the fee adjustment. Fourteen of the 19 EAM Portfolios had 100% Success Rates.

By contrast, to reach a 77.1% Success Rate, the average active portfolio would need an Alpha Gap of 443 bps.

Performance Metric 2: Relative Performance for Live EAM Portfolios

We next expanded the sample group back to all 34 EAM Portfolios and compared their relative performance to both their corresponding benchmarks and the actively managed fund peer groups. All performance is based on the date that each EAM Portfolio went into live production, through the end of November 2020.

Relative Performance: All EAM Portfolios

The results were compelling:

- 71% of the EAM Portfolios outperformed their benchmarks.

- EAM Portfolios outperformed 79% of fund peer groups.

- EAM Portfolios delivered annualized excess return of 920 bps versus their benchmarks.

- Only 11 of the 34 active peer groups outperformed over the same time periods as EAM portfolios.

Performance Metric 3: Implied Peer Group Rankings for Live EAM Portfolios

Live EAM Portfolios have handily outperformed the corresponding fund peer group averages. But how did EAM Portfolios outperform the elite funds within each category?

We created custom peer groups based on Morningstar Categories (e.g., Large Blend) and then mapped the trailing 12-month returns for the 19 EAM Portfolios with 12-month track records against their peer group. From this, we determined implied peer group rankings. Again, for comparison purposes, we deducted 85 bps from each EAM Portfolio’s return to simulate fees.

EAM Portfolios: Implied Peer Group Rankings

Again, the results were impressive.

- Sixteen of the 19 EAM Portfolios (84.2%) ranked within the top quartile, with one EAM Portfolio each in the second, third, and fourth quartiles.

- Of the 16 Portfolios in the top quartile: 14 ranked in the top decile, or the top three rows of the preceding chart, and 10 ranked in the top 2%, or the top row of the chart.

Put another way, 52.6% of the 19 EAM Portfolios with a 12-month history had an implied peer group ranking in the top 2%, after reducing returns by 85 bps.

None of the 10 largest fund managers as ranked by actively managed US equity fund AUM had 10 funds in the top 2% of these peer groups. In fact, these top firms did not collectively have 10 funds in the top 2%.

Performance Metric 4: Measuring the “True Nature” of EAM Portfolios

A single measurement rarely captures the essence of an item. But if the outputs from multiple approaches, with different sample sizes, time frames, and metrics, converge on similar results, then the essence of that item is coming into view.

That’s what we are seeing with EAM Portfolios. The live performance data demonstrates that EAM Portfolios have persistently outperformed their passive benchmarks and greatly outpaced traditional actively managed mutual funds. Moreover, the results of a 2018 study of 30,000 randomly constructed EAM Portfolios, detailed in the right-hand column below, are in line with these findings.

The “true nature” of Ensemble Active Management is thus coming into sharper focus:

- EAM Portfolios have outperformed standard passive benchmarks 70% to 75% of the time, and actively managed mutual funds 80% to 85% of the time.

- The 19 EAM Portfolios with at least a 12-month history had an average Success Rate of 77.1% against their benchmarks and 85.6% against their active peer group.

- The 34 EAM Portfolios in live production have outperformed their benchmarks 70.6% of the time, with an average annual excess return of more than 900 bps.

- These 34 EAM Portfolios also outperformed their peer groups 79.4% of the time.

Again, to put this data into perspective, the Alpha Gap for the traditional actively managed fund industry to achieve the 77.1% average Success Rate of live EAM Portfolios is 433 bps.

V. Implications for the Industry

This analysis confirms the active management industry has failed to beat its passive benchmarks. Moreover, the size of the Alpha Gap measurements shows how far behind active management has fallen. Absent radical change, it cannot catch up.

But there is hope. Ensemble Active Management is a viable blueprint to improve investment decision making and may be active management’s inevitable future. Adopting EAM will require existing investment firms to change, but the change is achievable. In addition to emphasizing quality strategies, the industry must now place a premium on generating a reasonable quantity of active strategies.

An easy first step? Instead of investment professionals collaborating on a single predictive engine, firms can split the teams into independent silos and construct the final portfolio using Ensemble Methods.

A big question is whether the incumbent investment firms will embrace EAM first and reap the benefits of early entry as Vanguard and BlackRock did with index funds and exchange-traded funds (ETF)s, respectively. Institutional investors have access to countless strategies today. Instead of treating them as sleeves in a large portfolio, they can extract the predictive engines from the underlying strategies and use Ensemble Methods to build their own EAM Portfolio. The same is true for large broker-dealers and scaled wealth managers. And the potential for technology firms to enter and make an impact is real.

To paraphrase Clayton M. Christensen in The Innovator’s Dilemma, incumbents are not entitled to retain market share as change and innovation sweep through an established industry.

Finally, successful active management matters. It matters to those in the investment management industry and to those advice industry professionals who are supported by successful actively managed portfolios. It matters most of all to the millions of investors around the world who need actively managed equity portfolios to provide for their future financial welfare.

Whether the industry is ready or not, Ensemble Active Management is coming.

Appendix 1

The Netflix Prize Case Study: Ensemble Methods in Practice

The Netflix Prize is an interesting example of the power of Ensemble Methods. In 2006, Netflix offered $1 million to the first team that could improve its proprietary Cinematch algorithm by 10%. Cinematch recommended content to Netflix customers based on what they previously watched and ranked. The competition attracted thousands of computer science grad students and coding professionals, and even such world-renowned research firms as AT&T Labs. Eventually, more than 40,000 teams from 186 countries submitted entries.

Initially, the entrants took a “single-expert” approach. Progress was immediate, albeit modest. Three teams outpaced Cinematch results by approximately 1% soon after the competition’s 2 October 2006 launch. By the end of the year, dozens of teams had eclipsed Cinematch, some by almost 5%. But then teams reached the limits of single-expert strategies, and progress ground to a halt.

The breakthrough came when teams began building “multi-expert” Ensembles from their own predictors. For example, Team Gravity created Ensembles from three of its internal algorithms and achieved an average 2.2% improvement over its three single-expert algorithms. It then improved its results an average of 3.6% by pairing the algorithms and then 4.5% over Cinematch after linking all three predictors.

Team Gravity Improved Results by Combining Algorithms

But Ensembles of three algorithms were nowhere near the scale of what other teams were attempting. By the end of 2007, the top results came from an AT&T Labs team: BellKor applied an Ensemble of 107 internal algorithms for an 8.43% improvement over Cinematch.

After almost three years, the 10% target was reached. On 18 September 2009, Netflix announced the winner, a “super-Ensemble” dubbed BellKor’s Pragmatic Chaos that combined three independent teams, BellKor, BigChaos, and Pragmatic Theory. Appropriately, the second place team was another super-Ensemble combination named The Ensemble.

Appendix 2

Statistical Comparison: EAM Portfolio vs. Corresponding Multi-Manager Portfolio

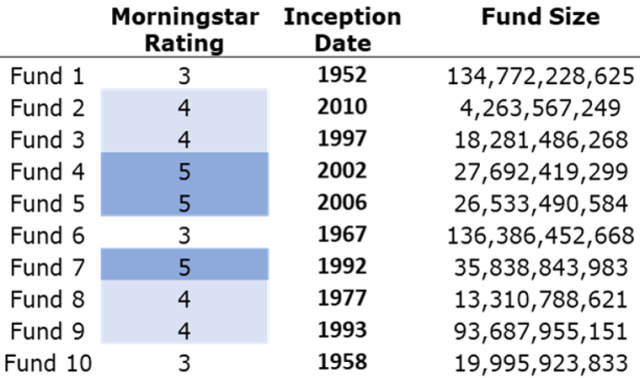

A family office launched the second of its two EAM Portfolios in May 2009. The portfolio was based on the predictive engines of 10 Large Blend funds and benchmarked against the S&P 500.

The general profile of the 10 funds are presented in the following chart. These funds varied widely by size and inception dates. Based on Morningstar’s five-point rating scale, they were all average to above average.

Profile of Mutual Funds

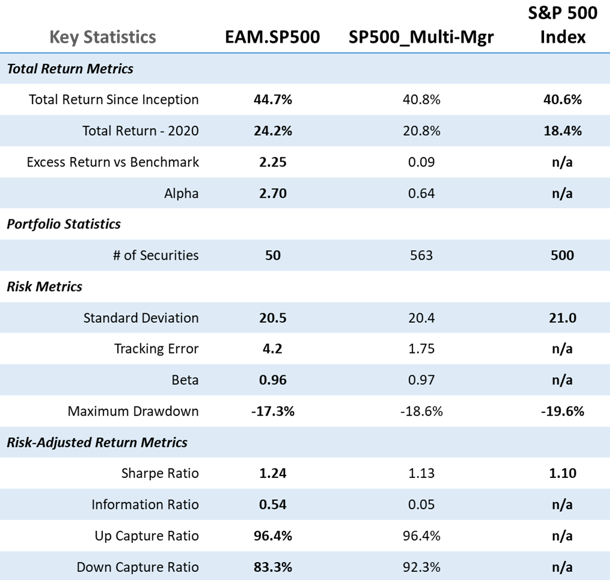

To better understand the difference between EAM and multi-manager portfolio construction techniques, Turing built a synthetic multi-manager portfolio from the same 10 underlying funds.

This multi-manager portfolio’s daily returns were generated from the daily average return of all 10 funds. In other words, it was rebalanced daily. The EAM Portfolio is based on actual performance data. (The EAM Portfolio’s performance was calculated using industry standard methodology for Model Portfolios, resulting in gross of fee returns. If a theoretical 85 bps were deducted to simulate fees, the summary conclusions would not change.)

Key Statistics: EAM Portfolio, Multi-Manager Portfolio, and Benchmark

- Portfolio Statistics show one critical distinction between the two active portfolios: The EAM Portfolio owned 50 stocks compared to the multi-manager portfolio’s 563 (as of December 2020).

- The EAM Portfolio generated superior investment returns, excess return, and alpha.

- The EAM Portfolio had similar overall risk metrics to the multi-manager portfolio and lower risk than the S&P 500.

- The EAM Portfolio also had superior risk-adjusted returns across all metrics.

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image credit: ©Getty Images/ Studio_3321

[ad_2]

Source link