GARP Investing: Golden or Garbage?

[ad_1]

Value vs. Growth

With their thousands of employees, suites of products, international reach, and legendary histories, General Electric (GE) and Amazon are true corporate empires. Of course, GE’s fortunes have lately been in decline while Amazon’s are ascendant. But the stocks of these two companies stand for more than just the old versus the new; they also represent a face-off between two investment styles: Value and Growth.

Most investors are inclined toward Value, a preference backed by ample academic research. But these days, picking GE, which trades at a significantly cheaper valuation than Amazon, would be challenging for most investors. The company has structural issues that are reflected in a declining share price and a slew of negative news stories, all of which would give one pause when considering the stock. Amazon has no such dilemmas and is decimating entire industries, secure in its status as the most valuable company on the planet.

Some investors have sought to bridge the Value–Growth divide through a hybrid strategy, opting for the growth at a reasonable price (GARP) approach popularized by Fidelity manager Peter Lynch. But if Value creates positive excess returns, as the research demonstrates, then Growth does largely the opposite, which would seem to cast doubt on GARP’s underlying logic. So how do GARP strategies perform in the US stock market?

Methodology

Definitions of GARP stocks can vary but are generally based on the price/earnings (P/E) to growth ratio (PEG), which divides the P/E ratio by the growth rate. In our analysis, we derive the PEG from the P/E ratio from the last 12 months of earnings and the three-year growth rate of earnings. Stocks that exhibit a PEG ratio below 1 are classified as GARP stocks. We focus on all US stocks with market capitalizations greater than $1 billion. Indices are rebalanced monthly, each transaction incurs costs of 10 basis points (bps), and stocks are weighted by their market cap.

Analyzing GARP Stocks

GARP stocks are selected by a combination of earnings growth and valuation. The idea is to identify those that sit somewhere between GE-like Value traps — cheap stocks with a bleak future — and overhyped and overvalued Growth stocks reminiscent of Amazon. Accordingly, we find that the earnings growth of GARP stocks is significantly above that of the market.

Three-Year Earnings Growth: GARP Stocks vs. All Stocks

Source: FactorResearch

Not only do GARP stocks show higher earnings growth than the market, but they also have lower valuations. The analysis shows median rather than average P/E multiples, which explains why the benchmark P/E multiples of all stocks are less extreme at certain periods — for example, during the tech bubble in 2000 — than in similar capital market research.

Valuation (PE Multiples): GARP Stocks vs. All Stocks

Source: FactorResearch

Does the stock market provide a sufficient number of companies that are growing earnings while trading at reasonable valuations? We find that, on average, 38% of all stocks exhibit a PEG ratio below 1, which is more than enough for security selection.

Stocks in the US Stock Market with PEG below 1

Source: FactorResearch

Broken down by sector, GARP stocks compose a relatively diversified universe. Some sectors, like financials and consumer discretionary, contribute more stocks relative to the benchmark of all stocks, while telecoms, utilities, and real estate contribute less. The latter three are asset heavy, exhibit only low earnings growth, and tend to trade at high P/E multiples given their bond-like features, so their PEG multiples rarely fall below 1.

GARP Stocks: Breakdown by Sector

Source: FactorResearch

GARP Stocks vs. the Stock Market

Investor interest in Value and Growth is driven by a desire to outperform the market. GARP stocks have indeed outperformed substantially since 1989. But that can be explained in part by simply excluding stocks with negative earnings. The PEG ratio calculation requires stocks to have positive earnings. When negative earnings stocks are filtered out, then the GARP stock outperformance declines substantially.

GARP Stocks vs. the US Stock Market

Source: FactorResearch

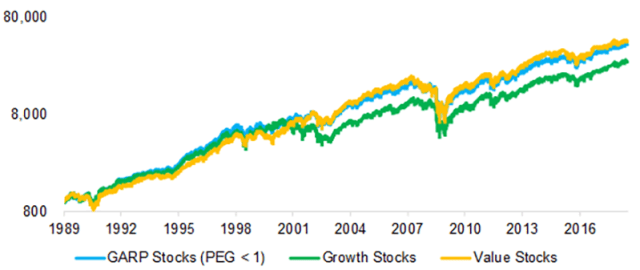

GARP — More Like Value or Growth?

Since GARP combines Value and Growth investing, we can benchmark GARP stocks to their Value and Growth counterparts. Here we define Value as a combination of price-to-book and P/E multiples and Growth as a combination of the three-year sales and earnings growth.

According to the analysis, a GARP approach seems to extract the best of both investment styles. Between 1989 and 2001, GARP and Growth outperformed Value, especially during the tech bubble between 1999 and 2001. However, when the tech bubble imploded and Growth started to underperform Value significantly, GARP stocks behaved more like Value stocks.

GARP vs. Growth and Value Stocks

Source: FactorResearch

This data demonstrates that GARP was an effective strategy since 1989, though how effective depends on the time frame. If we rebase the portfolios in 2000, then a pure Value portfolio would have worked better. Rebase the portfolios in 2010, and the market would have generated the highest annual returns, especially if negative earnings stocks are excluded.

GARP Performance across Different Time Periods

Source: FactorResearch

Further Thoughts

Fusing Value and Growth has an intuitive appeal but is somewhat at odds with academic research.

Our results suggest a GARP approach can generate enviable results, although how enviable depends on the observation period.

Perhaps the strategy’s key benefit is forcing investors to adopt a systematic framework so they can allocate to exciting growth stories — the rising Amazons — albeit only when they are trading at reasonable valuations.

For more insights from Nicolas Rabener and the Factor Research team, sign up for their email newsletter.

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image credit: ©Getty Images/Endai Huedl

[ad_2]

Source link